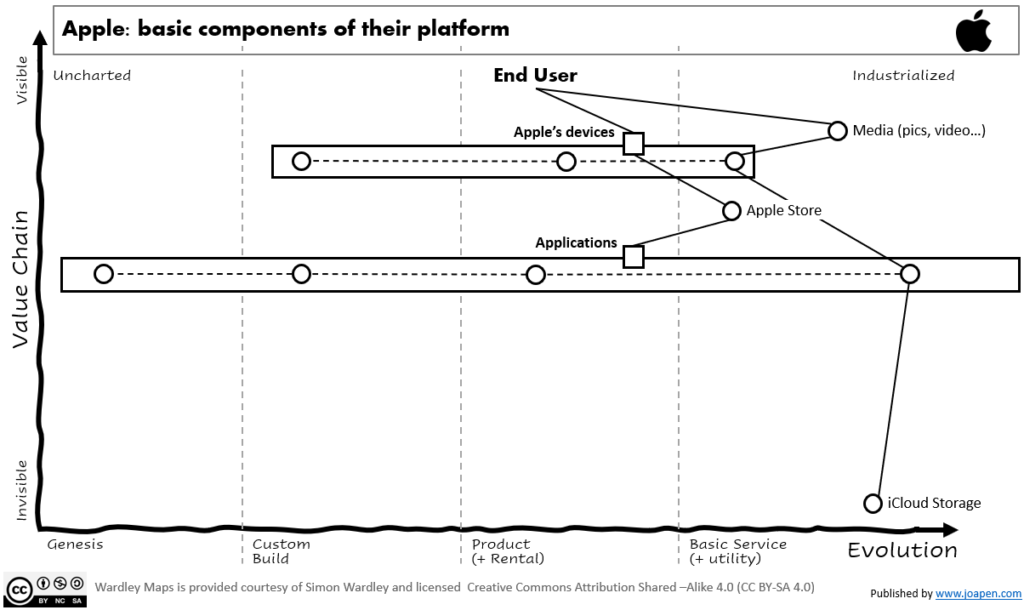

Apple ecosystem is composed by many elements.

- The devices: are the main ones and they enabled the creation of a platform where the user experience happens.

- The applications: The iPhone was in its inception offered not as a mobile phone, but as a device that offered many applications. All this is now natural to us as consumers, but in 2009 it was disruptive. All this happens thanks to the Apple Store where Apple and third players implement solutions that satisfy user needs and contribute to the use of the Apple’s devices and other services.

- iCloud, security and other services: The Apple’s world is extense and composed by many elements that ensure you do not need to exit to consume services (at least the main ones).

This basic components could be drawn on a map like this:

Notice that I have drawn the devices and the applications as pipelines, as there are many of them and there is evolution in each one of these major elements. For instance:

- Related to devices: we can have iPhone as mature device, AirPods as a major product being consumed today, and TV & Home as small players on this ecosystem.

- Related to applications: we could have millions of apps that try to survive in a world where attention is limited. I will focus on this pipeline in the next section.

Gameplays to protect their platform

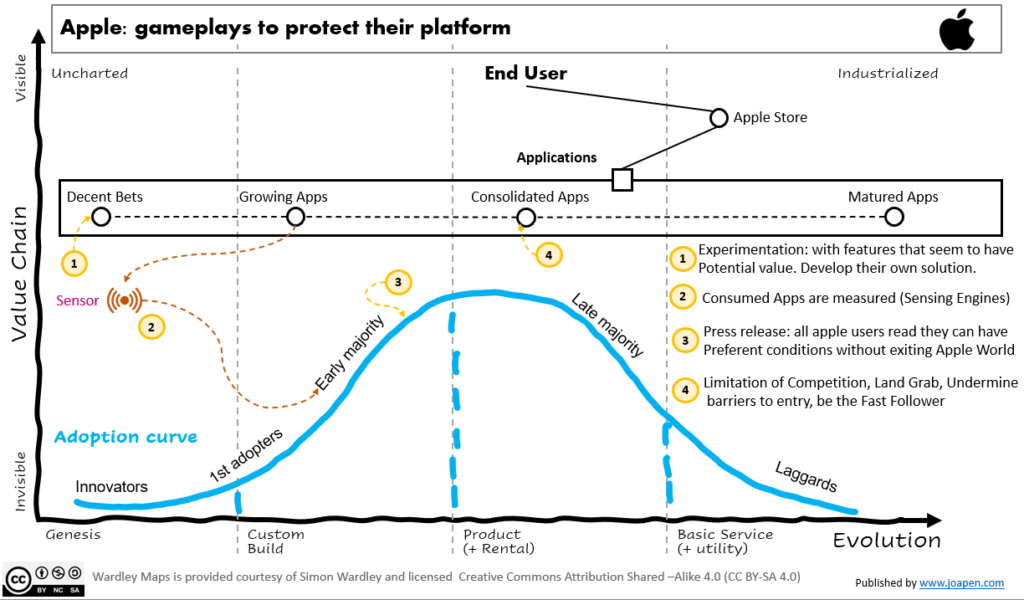

Let’s consider the applications space as the main battlefield where the user is consuming services. We then have the Apple Store as the entry of the users to install apps and consume their services.

Who can know all data about downloads, consumption of all this? Apple

In the long term, Apple want the user to consume as much from their platform as possible, this includes the Apple services as iCloud, iPay, etc. So the protection of the platform and the use of the platform in the better way for Apple is one of the key purposes in Apple.

To do that, Apple does not only have to implement applications, but they have to be able to position themselves as main players so they protect the strength of their platform.

How do they protect their platform?

In my view, there is a generic approach that is followed in all parts of the application catalog and there are specific gameplays in major fields as payments, health and social media.

Let’s review the generic approach to protect the platform

I have done a weird Wardley Map, adding the adoption curve to the standard map, so it helps to remember how the consumption evolves (there’s co-evolution of practices and technology).

In the first side, I have added the Applications pipeline, which catalog is composed by applications in all stages defined in a Wardley Map.

Apple has the ability to experiment and gather information about the use of the applications, to me they are listening the consumption of applications and features and they are experimenting (#1) the way to offer by themselves (when there is a business reason behind it).

They focus the appliance of sensing engines (#2) on applications that have higher growth in relevant segments for Apple (social media, finance, health…). If some of these applications sector presents some weak signals that could turn into massive consumptions, they turn their experiments in formal solutions, so they can be part of the competition and learn about how they really are consumed (you cannot separate strategy from execution, you need to learn the reality of the user consumption).

In case they want to accelerate the visibility of their product, they orchestrate the release of news (#3) related to that in a way that all Apple users understand the existence of a new Apple service. Press releases with the adequate data is more effective and cheap than a marketing campaign, and Apple has the brand to provoke thousand of newspaper’s headlines.

All this contribute in the space of the consolidated applications to (#4):

- Limitation of competition: as there is a new piece of revenue, Apple want their part.

- Land Grab: they conquer new areas of user needs with their own services.

- Undermine barriers to entry: they protect their platform.

- Be the Fast Follower: they let others to take the risk of being the first mover and really check that the user need is a real need that can be massively consumed.

Apple: generic gameplays to protect their platform

Specific example in the payments space

In this article titled: Apple Will Handle Lending Itself With New Pay Later Service, Apple executes the action #3 I mentioned below.

In addition to the generic protection approach mentioned before Apple is adding some other gameplays to the equation:

- Apple is having an alliance with Mastercard (they are using their payment credentials).

- Apple continues working with Core Card Corp. (alliance).

- Apple’s has acquired Credit Kudos Ltd. (from UK) for potential expansion out of US. Typically all US companies do the first international expansion in Europe.

- Apple uses the 200B$ cash as “fish hook” to generate headlines across the finance world. In fact they are writing a lot about this excessive mass of cash. Some of them consider this big amount of billions are underused (more headlines).

Looking with perspective

In the short run, for the “buy now, pay later” context Affirm Holdings and Klarna Bank are the potential companies affected in a negative way, but for the long run, on the “payments” contexts, to my honest opinion Visa, Mastercard, Core Card Corp. and other payment solutions are the impacted by this long term strategy.

This is not the first battle in the payment space, neither the last one. In the post the payment war in the mobile app ecosystem, I comment some elements of this long term war.