Permanent open market operations (POMO), how it works

How the Permanent Open Market Operations (POMO) works

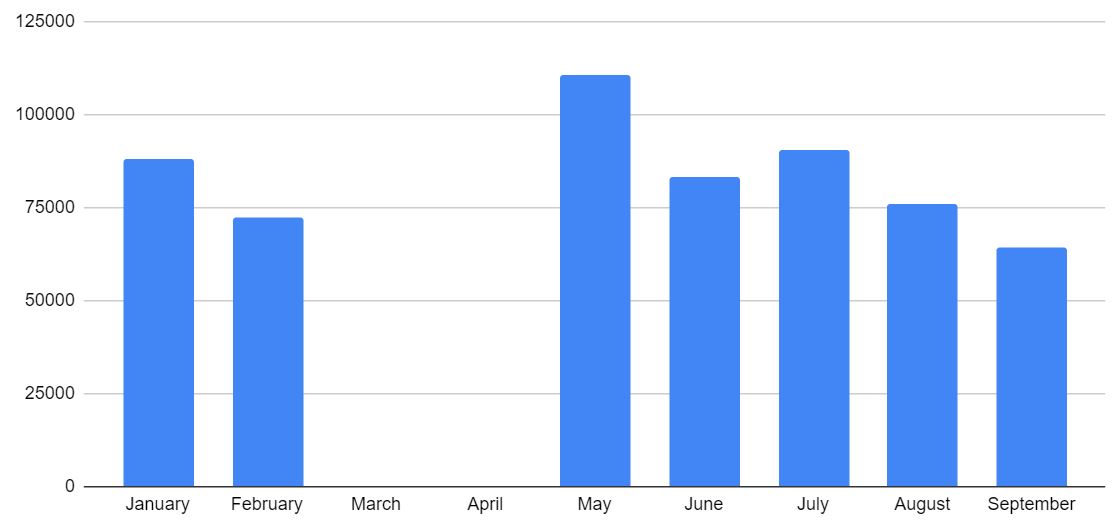

Just a place to write

How the Permanent Open Market Operations (POMO) works

I have invested some hours learning about Quantopian environment and the basic concepts around the platform. The environment is very powerful, so I wanted to gain some basic clarity of the basis. Quantopian platform It consists of several linked components, where the main ones are: Quantopian Research platform is an IPython notebook used for research and … Read more

I have read a couple of texts related to the simple moving average or rolling average, this one explains the basis and the main values used. I have done some tests and I have compared them to understand the use better. The different articles always have some tips about this analysis: Do not operate based … Read more