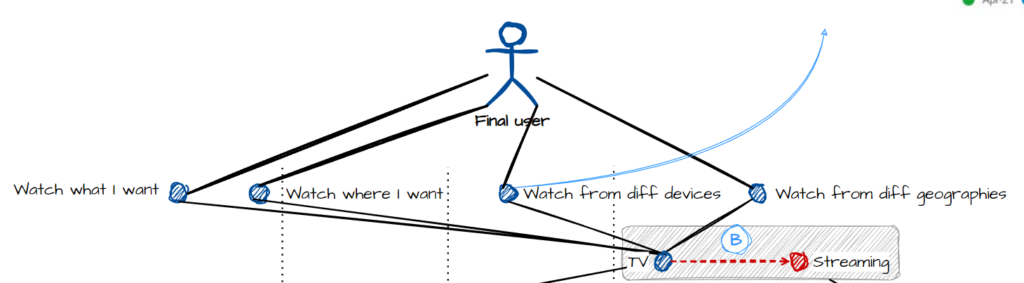

The user is the center of the whole thing. Technology has made the whole ecosystem has changed and that pace of change is faster and faster.

We are moving in the last 10 years from a TV model to a streaming model where in the future they are going to co-live. To consider:

- TV has a strong presence, specially on live events, news and certain parts of population.

- New generations consume more streaming than TV.

- The combination of needs made the granularity of the consumption is more and more complex, which makes the construction of capabilities more complex too. To be right seem more easy than ever (because we have data), but it’s just the opposite thing.

- How are both models co-living?, How both models are going to evolve?, will see.

The point “B” is right now in a direction but this will take years of different layers of diffusion to a new situation for the ecosystem. Strong contracts as Sport contracts in countries as US are a huge volume of the revenue and TV consumption (For instance NBA League Pass).

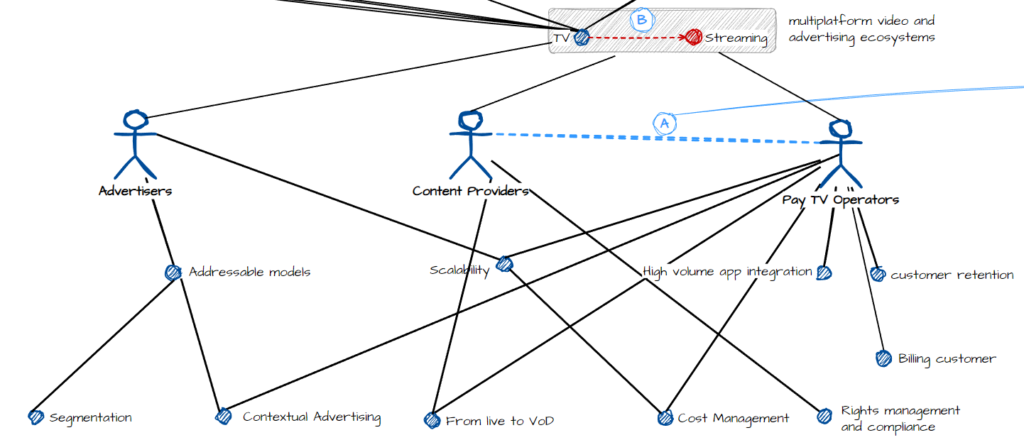

Multiplatform video and advertising ecosystems

This is a value chain of needs with the main 3 players the industry recognizes:

All these needs are required by the players that compete in the ecosystem.

The 3 major players:

- Content providers want to develop closer, direct-to-consumer relationships across devices.

- Pay TV operators want to become super-aggregators that bring disparate services into a unified experience.

- Advertisers want addressable, data-driven operations that target and tailor messages at the screen level.

Here we can ask ourselves many questions:

- How do they resolve the complexity of attending the user?

- How do they make profits with these services?

- What are the main flows of capital happening between components?

- How the current contracts limit the evolution of the ecosystem?

- How the renewal of major contracts change the competition between parties?

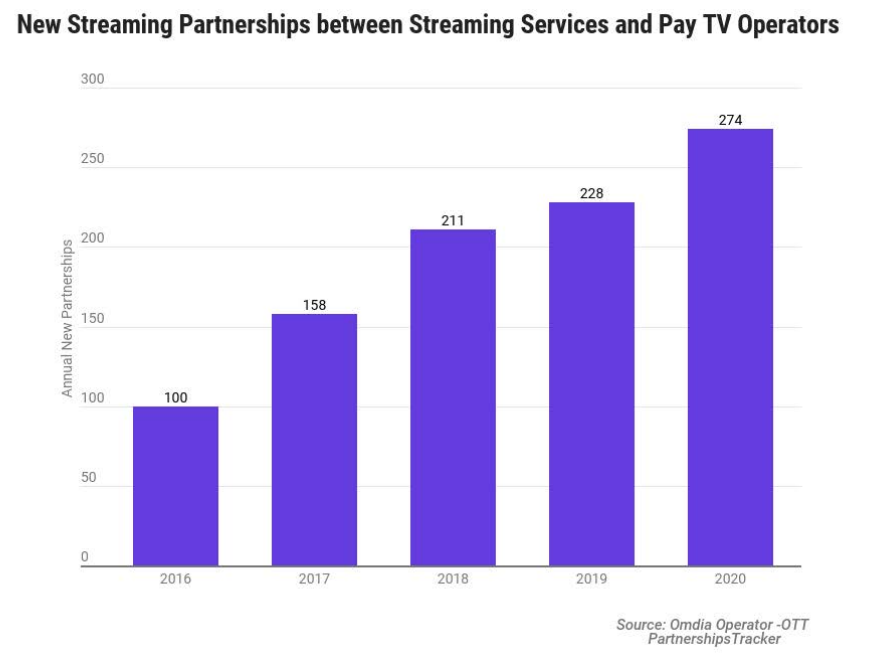

The “A” indicates the partnership between Pay TV Operators and Streaming Services (US only).

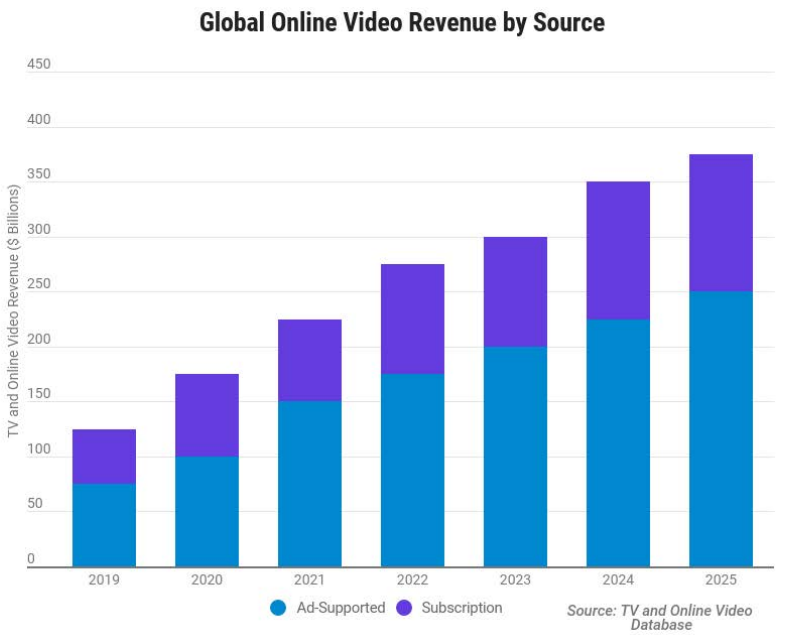

The revenue continue growing and the forecast the industry provides continue being positive in terms of growth:

Technological challenges

The three major challenges for the tech side of the companies come from the needs:

- Scalability,

- High volume app integration and

- Segmentation

Ideally:

- You are able to attend the stable demand with your on-premises infrastructure and attend the high peaks with scaling capabilities on the cloud.

- You are able to deploy changes on the different devices in a fast pace approach and without outages for the users.

- You are able to digest, classify, divide content, track details of consumption and build patterns of behavior that enable advertisers to better work on your environment.

The reality is different, each environment has its own complexities, but in general is accepted these major moves on the tech side of the industry.

On-premises and cloud

Streaming services and video services are served with high availability and when millions of users demand something you have to provide it.

To have all infrastructure by yourself is simply not affordable, so to have the right combination of public-private cloud or hybrid model is key.

Monolithic vs distributed architecture

There are many workflows that are still monolithic and to turn them into distributed ones takes time. On the other hand probably there are systems that does not make sense to upgrade. But how?

The main action I have read is through the use of scalable microservices. It’s interesting I have not read any trend about Serverless approach.

Scaling up the Prime Video audio/video monitoring service and reducing costs by 90%

This week this article from Amazon Prime was published. They explained how they have been adapting their systems to enable themselves to be more profitable, efficient and being able to increase the usage-tracking to all viewers.

Definitely, his is not an easy business.